2015/09/18 TrendView VIDEO: Global View (early)

© 2015 ROHR International, Inc. All International rights reserved.

The analysis videos are reserved for Gold and Platinum Subscribers

TrendView VIDEO ANALYSIS & OUTLOOK: Friday, September 18, 2015 (early)

Global View: All Markets

Global View: All Markets

‘Fed Dread’ turned out to be the issue we thought it might be for equities, yet not in a way we imagined. The FOMC did not just hold steady where it might have been more productive to provide a ‘fractional’ rate hike (see Thursday’s Commentary post on that.) It also provided a very downbeat assessment of not just the global economy but also the horizon for the Fed to see its inflation target hit… not until 2018!? Whatever discussion the Fed now provides on the potential for rates to rise this year versus waiting until 2016, there are other questions which come to mind.

As we discussed the Fed’s need to avoid it in yesterday’s Commentary, we ask again whether this is now a case of it being the “proverbial deer caught in the ‘waiting for perfection’ headlights”? Or is something more troubling afoot in the land? While the Fed would be rue to admit it, and most analysts and financial media commentators are not raising the issue, might this be the beginning of a stark realization?

Is it possible that all the massive US and international Quantitative Easing (QE) is actually failing to return the world to more robust growth? We have been on this topic for a long time now, becoming increasingly pointed this year on the lack of reforms being a real issue (see below for more on that.) While it is not the central bankers ‘fault’ per se, it is their lack of pressure on the political class to do its part that is now telling. The politicians have been glad to accept QE as a giant gift, relieving them of the pressure to do any heavy lifting on the complimentary reforms necessary to restore real economic growth.

_____________________________________________________________

Video Timeline: It begins with macro (i.e. fundamental influences) mention of the recent mixed data becoming weaker once again as noted above along with China and Emerging Markets still a problem. That much was confirmed by the Fed yesterday. Even the ECB potential QE expansion two weeks ago did not help. With much of the data this week below estimate as well, the Fed’s downbeat assessment would seem to be in line with little inflation and troubling weak US wages, Retail Sales, Industrial Production and Philly Fed.

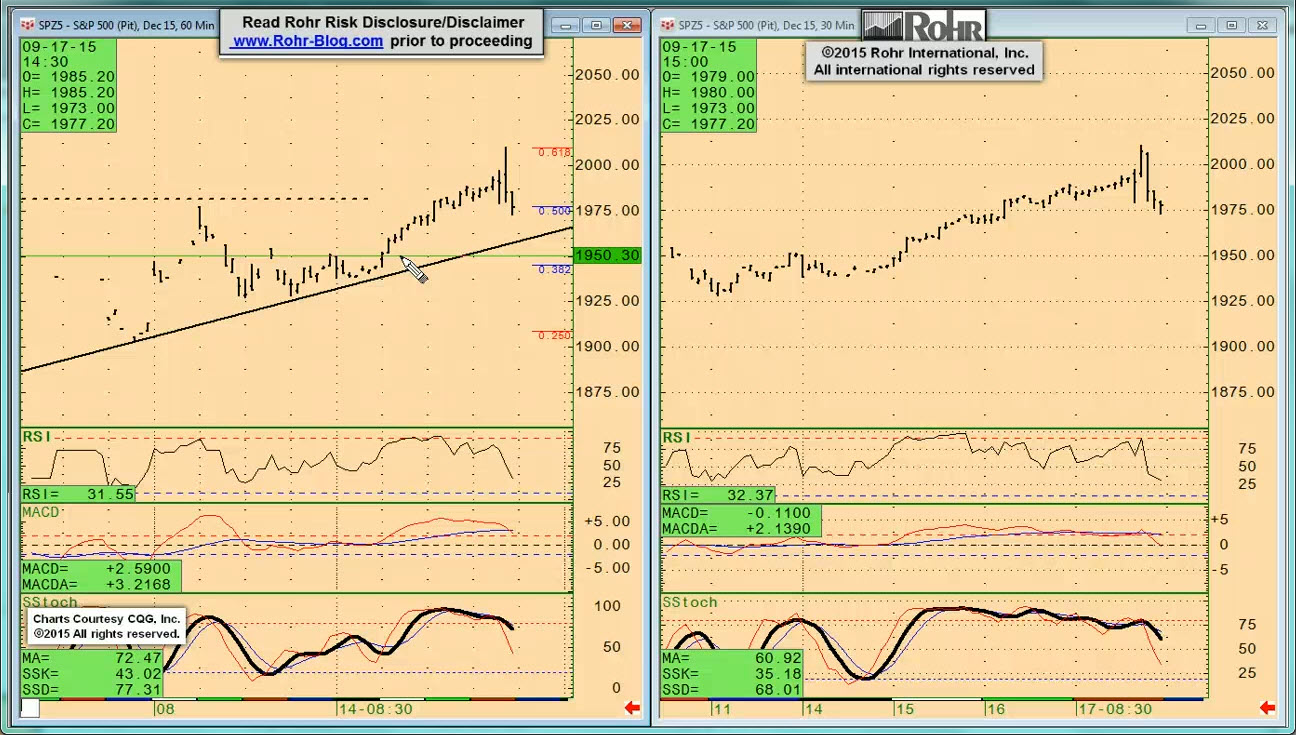

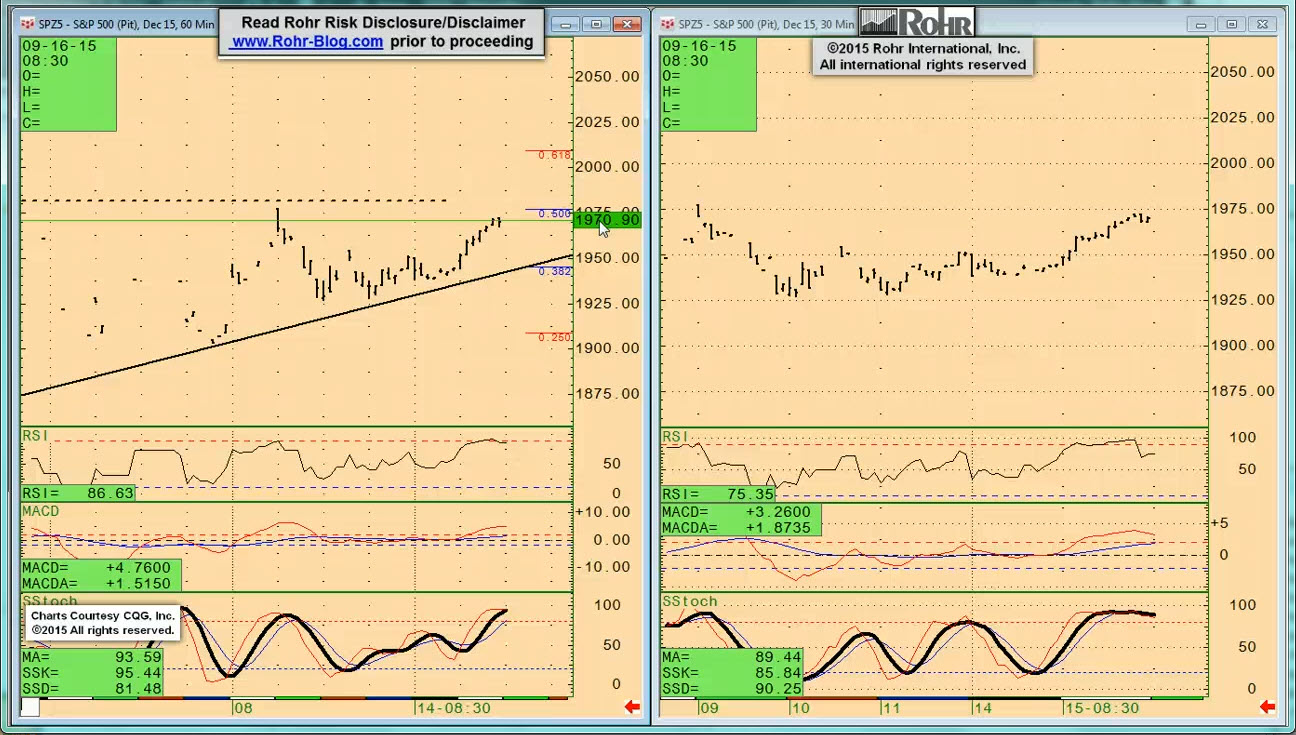

It moves on to S&P 500 FUTURE short-term indications at 02:30 and intermediate term view at 06:15, OTHER EQUITIES from 08:30, GOVVIES analysis beginning at 12:45 (with the DECEMBER BUND FUTURE at 17:45) and SHORT MONEY FORWARDS at 20:00. FOREIGN EXCHANGE covers the US DOLLAR INDEX at 23:15, EUROPE at 25:30 and ASIA at 28:00, followed by the CROSS RATES at 30:00 and a return to S&P 500 FUTURE short term view at 34:15. As this is an especially extensive analysis due to the extended fundamental discussion and futures expirations, even more so than usual we suggest using the timeline cursor to access analysis most relevant for you.

_____________________________________________________________

Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion and TrendView Video Analysis and General Update. Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion.

2015/09/22 TrendView VIDEO: Global View (early)

2015/09/22 TrendView VIDEO: Global View (early)

© 2015 ROHR International, Inc. All International rights reserved.

The analysis videos are reserved for Gold and Platinum Subscribers

TrendView VIDEO ANALYSIS & OUTLOOK: Tuesday, September 22, 2015 (early)

As noted last Friday morning, ‘Fed Dread’ turned out to be the issue we thought it might be for equities, yet not in a way we imagined. The FOMC did not just hold rather than provide a likely more productive ‘fractional’ rate hike (see Thursday’s Commentary post on that.) It also provided a very downbeat assessment of not just the global economy but also the horizon for the Fed to see its inflation target hit… not until 2018!? Whatever discussion the Fed now provides on the potential for rates to rise this year versus waiting until 2016, there are other questions which come to mind.

As we had suggested previous, is this now a case of the Fed it being the “proverbial deer caught in the ‘waiting for perfection’ headlights”? Or is something more troubling afoot in the land? While the Fed is rue to admit it, and most financial media commentators and analysts are not raising the issue, might this be the beginning of a stark realization?

Is it possible that all the massive US and international Quantitative Easing (QE) is actually failing to restore robust growth? While we have been on this topic for a long time now, we explored it again in Friday’s Market Observations (updated after the US Close.) Rather than a regular technical trend update, the early part of Friday’s post also links back to important OECD Composite Leading Indicators from earlier this month, and how the data has weakened to reinforce its weak view. The Market Observations include discussion of the typical ‘FOMC Friendly’ anticipation and subsequent weakening of equities.

_____________________________________________________________

Video Timeline: It begins with macro (i.e. fundamental influences) mention of the recent mixed data becoming weaker once again as noted above along with China and Emerging Markets still a problem. That much was confirmed by the Fed Thursday. Even the ECB potential QE expansion three weeks ago did not help. With much of the data last week below estimate as well, the Fed’s downbeat assessment would seem to be in line with little inflation and other weak data as we head for global Advance PMIs Wednesday, German IFO and US Durable Goods Thursday and the US GDP revision on Friday.

It moves on to S&P 500 FUTURE short-term indications at 02:45 and intermediate term view at 05:30, OTHER EQUITIES from 07:45, GOVVIES analysis beginning at 12:15 (with the DECEMBER BUND FUTURE at 16:15) and SHORT MONEY FORWARDS at 18:30. FOREIGN EXCHANGE covers the US DOLLAR INDEX at 21:30, EUROPE at 23:15 and ASIA at 25:45, followed by the CROSS RATES at 27:15 and a return to S&P 500 FUTURE short term view at 31:00. As this is an especially extensive analysis due to the extended fundamental discussion and futures expirations, even more so than usual we suggest using the timeline cursor to access the analysis most relevant for you.

_____________________________________________________________

Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion and TrendView Video Analysis and General Update. Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion.

Read more...