2020/04/19 Commentary: Snatching Defeat from the Jaws of Victory

© 2020 ROHR International, Inc. All International rights reserved.

Extended Trend Assessments reserved for Platinum Subscribers

COMMENTARY: Sunday, April 19, 2020

Both sides in the US government COVID-19 response seem to be working against their own interest. It may seem we are overly focused on US politics now. Yet they are critical due to US economic factors… and by extension the market impact.

Both sides in the US government COVID-19 response seem to be working against their own interest. It may seem we are overly focused on US politics now. Yet they are critical due to US economic factors… and by extension the market impact.

And as noted in last Thursday’s ‘We Call ‘Em the Way We See ‘Em’ research, complaints from select Trump supporters that some of our analysis seemed ‘anti-Trump’ is laughable. We are equal-opportunity critics, and are more than happy to highlight misguided assertions from anyone, including central banks, governments, corporate executives, and so on. Our extended discourse on that in last Thursday’s research note included the overview of how we did so in all previous serious market failures going back to 1987, 2000 and 2008.

Misguided Democratic Agenda Push

Back to the present again for non-US readers, recent actions and communication are classic examples in American politics of one side having an edge but then striving mightily to ‘snatch defeat from the jaws of victory’. Last Tuesday we cited Senator Rubio's disparagement of the Democratic House leadership’s refusal to support an automatic extension of the Paycheck Protection Program (PPP.)

To wit, (paraphrased) “...imagine the impact on the public psyche if they are told a program that was at least partially effective is being shut down due to Congress not being able to agree on providing more money for something that is already in place and functioning.” While we do not always agree with them, it would seem the Republicans had a legitimate point in this case.

And if Speaker Pelosi and her House comrades wanted more money for hospitals and very small businesses, they could have easily floated a new bill in the House. She would have had the backing of her Democratic majority, and the Republicans would likely have gone along.

Yet there is a political dynamic here: They want to have their demands included to create talking points for the election campaign into this November: their changes made it ‘better’.

Is this a great country… or what? Yet that may be moot, as the Republicans have capitulated on allowing for some additional Democratic demands for funding for other sectors, and promised future funding for state and local governments in separate bills. Good for them for not letting fragile small businesses be even more nervous on the program and susceptible to failure for lack of funding.

Trump Still Testy on Testing

Yet our greater criticism wheels back around to the Republicans, and specifically the still incorrect missives from Dear Leader Trump on ‘testing’. He has continued for a long time (in COVID-19 pandemic evolution terms) to assert the US has a strong infection testing facility. This was not true on March 6th when he clearly (mis)stated, “Anybody who needs a test, gets a test…” (http://bit.ly/3cUM2dm.)

While one might think that a month-and-a-half later that might be accurate, it is still not the case; at least not on the scale necessary to move toward his highly touted staged reopening of the US economy. In fact, Governors from both sides of the political aisle were all over the Sunday political analysis shows decrying Trump’s misguided claims, Republicans as well as Democrats.

The most damning likely came from a fellow Trump Republican Party member, who has praised the federal government for some things they have indeed done well. That is Maryland’s respected Governor Larry Hogan, also the Chair of the National Governors Association. While appearing on various Sunday shows, his most telling perspectives and points were derived from an extended interview on Jake Tapper’s CNN State of the Union (https://cnn.it/2RTdwHp.)

Governors Have Legitimate Issues

Proceeding through various topics, Tapper got Hogan’s responses Democrats holding up that PPP funding (01:00), noting that the governors did not want to have funding for their states delay the funding for small businesses. Hogan went on to note (02:30) that the President’s own guidelines are conditions that are not being met in his state (and many others.)

And regarding Trump’s assertion that the Governors need to get more aggressive and are dragging their feet where they already have ample testing ability (03:30-05:30), Hogan is very pointed: After video clips of Trump and Pence making those assertions on the availability of ample testing availability, Hogan first says that this has been a complaint of his since the spread of the novel coronavirus started, and he is hearing the same from Governors on both sides of the aisle every single day.

Then there was this…

“...to try to push this off to say that the Governors have plenty of testing and they should just get to work on testing, somehow we are not doing our job, is just ‘absolutely false’.” (Our additional punctuation) “Every Governor in America has been pushing and fighting and clawing to get more tests…” So there you have it.

What Kind of Testing?

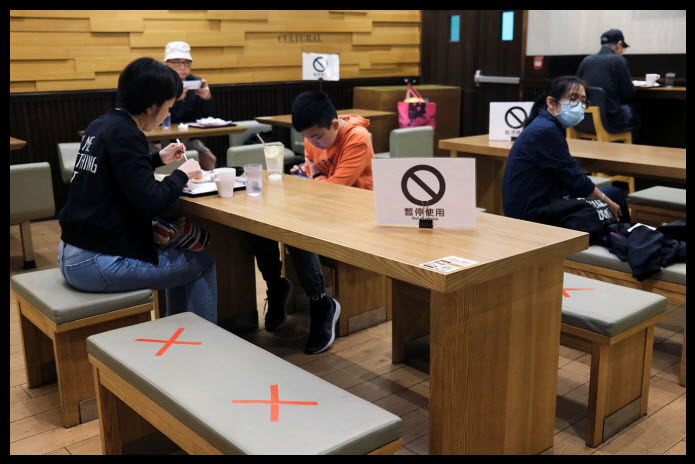

The other aspect that has been sorely lacking is any indication on the type of tests the federal government says it is ramping up at present. Are they the same tests which we have already had? Our understanding is that those were the 4-5 day results tests.

Well, those are not very effective for re-opening an economy where there will be close quarters everywhere from factory floors to the dining, hospitality and travel businesses. That delay will be an insurmountable hurdle.

Pelosi Only Public Voice on This

And the one person in all of government we have heard express this in terms that go to the crux of the matter is none other than Speaker Pelosi. In her Fox News Sunday interview with Chris Wallace she inquired, “Where are the ‘rapid’ tests?” (Once again our additional punctuation)

This is the real point even beyond the per capita deficient US testing that Trump continues to deny: There needs to be sustained, regular, extensive testing, even including the asymptomatic.

The two-week asymptomatic nature of this particular virus was a problem we highlighted as a major market concern from when awareness of that aspect first appeared back in late-January (see our January 27th “The ‘Known Unknown’ Carries the Day” research note for more.)

The only way to address this is the ‘rapid’ tests. Ironically, as we noted last week Tuesday, there seems to be only one place to get a rapid response novel coronavirus test right now: Wuhan.

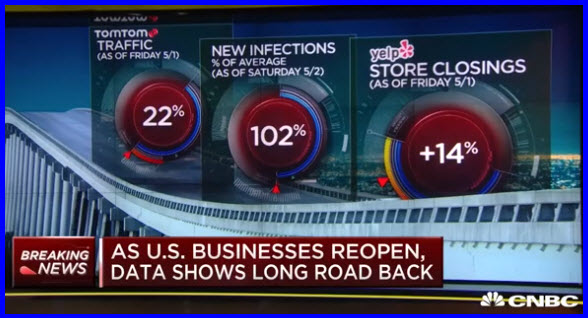

Sustained US Equities Skepticism (Updated Monday)

And this is why we remain skeptical of US EQUITIES overall, even though they might be able to rally further once they shake off this morning’s Crude Oil shock (more below.) More government programs and central bank largesse might encourage more near-term hope.

Authorized Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion. Non-subscribers click the top menu Subscription Echelons & Fees tab to review your options. Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to also access the Extended Trend Assessment as well.

Read more...