2015/12/02 TrendView VIDEO: Global View (early)

© 2015 ROHR International, Inc. All International rights reserved.

The analysis videos are reserved for Gold and Platinum Subscribers

TrendView VIDEO ANALYSIS & OUTLOOK: Wednesday, December 2, 2015 (early)

Global View: All Markets

Global View: All Markets

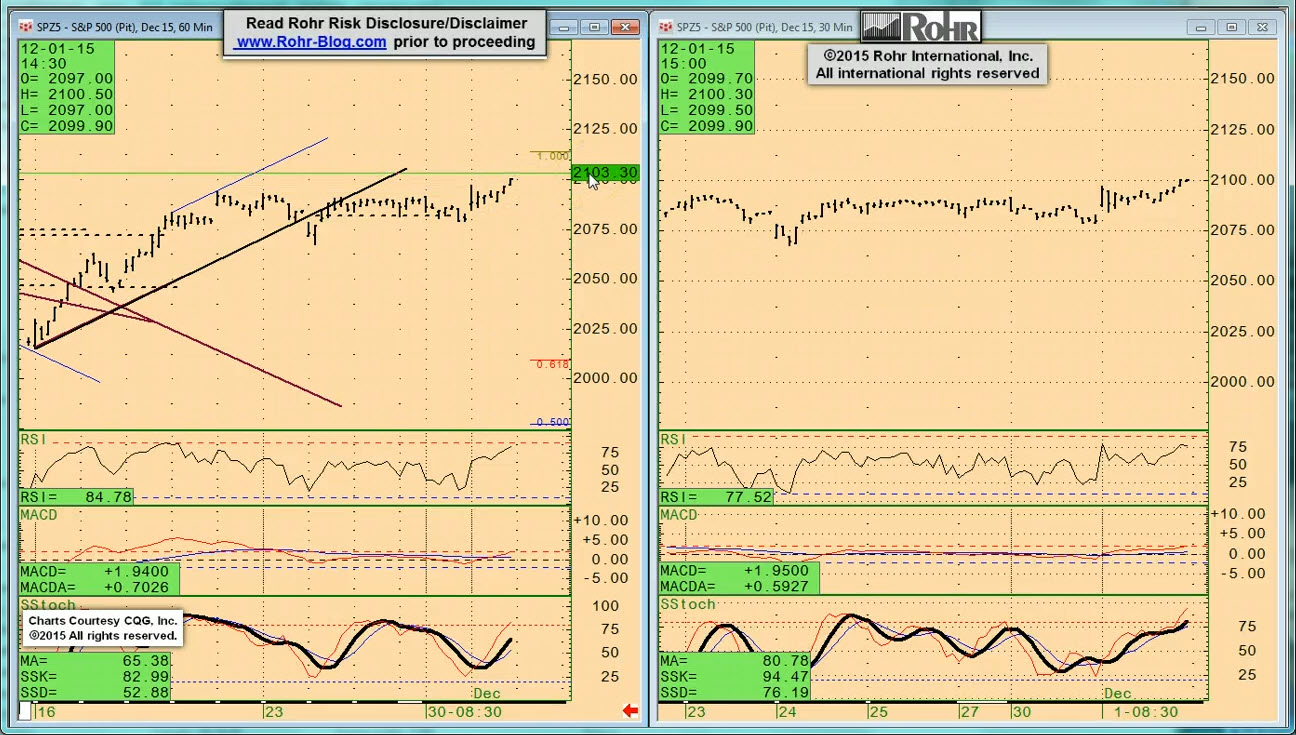

There is much that is still the same as last week’s analysis of the overall psychology in all asset classes. In spite of the constant drum beat from most of the Fed’s minions, the weak spots in US economic data (ISM Manufacturing comes to mind) leave a sense that the potential first rate hike in six years two weeks from today remains more problematic than they suggest. Possibly they will hike, yet provide quite a bit of ‘spin’ on how this rate rise cycle will be far more gradual than previous. It may even leave the feeling it is just an ‘adjustment’, or effectively a ‘one and done’ increase (even if they would never say anything like that.)

Then there is the ‘Super Mario’ factor, as ECB President Draghi holds the next post-rate decision press conference Thursday morning from an hour prior to US equities opening. Fed Chair Yellen’s Congressional Joint Economic Committee chat begins shortly after the ECB press conference. In all of that there are grounds to believe that equities remaining so firm on such mixed-to-weak data are indeed a ‘bad news is good news’ market again.

And while we remain skeptical of equities overall, since the top of last week we reminded everyone that the Santa Claus (more like ‘Santa Portfolio Manager’) rally influence was about to begin. As it is more so a ‘steady’ year than a significant gain situation, this may not amount to much more than the Santa ‘resilient underpinning’ rather than ‘rally’. Yet it is important to note this still means a tendency toward willing buyers on selloffs. For more on ‘Santa Portfolio Manager’ that we remind folks is actually the case every year (at least in the firm-strong ones) see last November’s post on that.

_____________________________________________________________

Video Timeline: It begins with macro (i.e. fundamental influences) mention of the factors noted above along with the return to weaker data in the US last week, including Durable Goods, New Home Sales and Michigan Sentiment. The weakness of the Chinese and US Manufacturing PMI’s is a cautionary indication along with very weak Canadian GDP. That said, the ADP Employment report was stronger than expected, and the question into all of the central bank influences for the balance of the week will be whether that is a credible indication that the US Employment report will be better than expected again this month?

It moves on to S&P 500 FUTURE short-term at 03:15 and intermediate term view at 06:45, OTHER EQUITIES from 09:45, GOVVIES beginning at 13:00 (with the DECEMBER BUND FUTURE at 15:45) and SHORT MONEY FORWARDS from 18:30. FOREIGN EXCHANGE covers the US DOLLAR INDEX at 21:00, EUROPE at 22:45 and ASIA at 25:00, followed by the CROSS RATES at 27:30 and a return to S&P 500 FUTURE short term view at 29:30. We suggest using the timeline cursor to access analysis most relevant for you.

_____________________________________________________________

Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion and TrendView Video Analysis and General Update. Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion.

2015/12/03 TrendView VIDEO: Concise Highlights (early)

2015/12/03 TrendView VIDEO: Concise Highlights (early)

© 2015 ROHR International, Inc. All International rights reserved.

The analysis videos are reserved for Gold and Platinum Subscribers

TrendView VIDEO ANALYSIS & OUTLOOK: Thursday, December 3, 2015 (early)

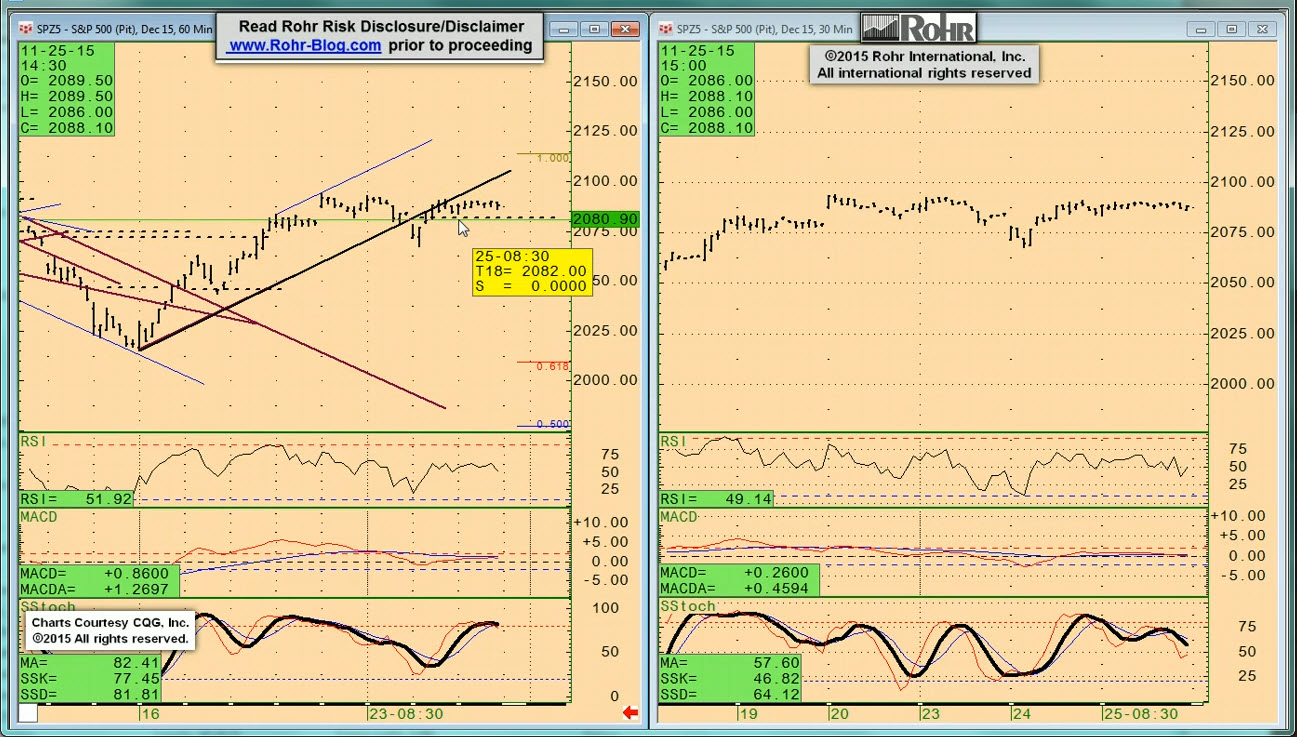

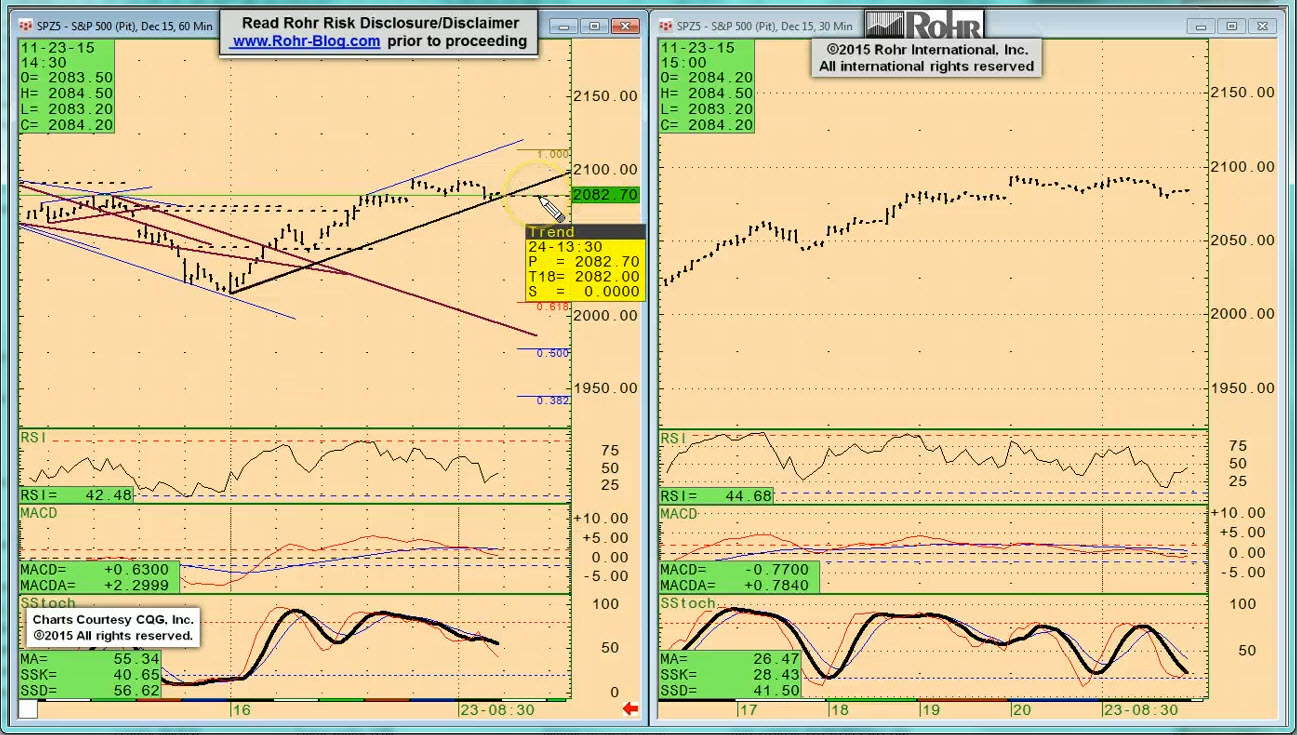

There is much that is still the same as Wednesday morning’s analysis in spite of the sharp swings in response to the next shootings in San Bernardino. However much these repeated disruptions bring sharp temporary weakness to the equities, the market seems to rebound as soon as it is established that they are not part of some broader attack. That said, our sympathy goes out to the victims of yet another human tragedy, even if it once again did not turn out to be an economic or market tragedy (as we have noted repeatedly.)

And the overall psychology in all asset classes remains the same. In spite of the constant drum beat from most of the Fed’s minions, the weak spots in US economic data (ISM Manufacturing comes to mind) leave a sense that the potential first rate hike in six years remains more contentious than they suggest. Possibly they will hike, yet provide quite a bit of ‘spin’ on how this rate rise cycle will be far more gradual than previous.

Then there is the ‘Super Mario’ factor, as ECB President Draghi holds the next post-rate decision press conference in a little while that lasts until the US equities opening. And Fed Chair Yellen’s Congressional Joint Economic Committee chat begins shortly after that. According to many analysts this is the extension of the Great Divergence that will see the euro weaken further and the US dollar strengthen significantly. As with many of these expectations, there is a question over whether much of the influence of the interest rate differential is already priced into current market levels. That is even more so the case now, as the strength of the US dollar is creating significant headwinds for the US economy.

_____________________________________________________________

Video Timeline: It begins with macro (i.e. fundamental influences) mention of the factors noted above along with the return to weaker data in the US last week, including Durable Goods, New Home Sales and Michigan Sentiment. The weakness of the Chinese and US Manufacturing PMI’s is a cautionary indication along with very weak Canadian GDP. That said, the ADP Employment report was stronger than expected, and the question into all of the central bank influences for the balance of the week will be whether that is a credible indication that the US Employment report will be better than expected again this month?

It moves on to S&P 500 FUTURE short-term view at 04:00 and intermediate term at 07:45 with OTHER EQUITIES from 09:30 and only mention of GOVVIES from 10:15 including discussion of the BUND at 11:00, and SHORT MONEY FORWARDS from 12:15. Foreign exchange is also only mentioned, with US DOLLAR INDEX at 12:45, Europe at 13:30, ASIA at 14:15 and CROSS RATES that are mostly steady yet with a strong Australian dollar and weak euro at 15:00 prior to returning to the S&P 500 FUTURE short term view at 16:15.

_____________________________________________________________

Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion and TrendView Video Analysis and General Update. Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion.

Read more...