2015/08/21 TrendView VIDEO: Global View (early)

© 2015 ROHR International, Inc. All International rights reserved.

The analysis videos are reserved for Gold and Platinum Subscribers

TrendView VIDEO ANALYSIS & OUTLOOK: Friday, August 21, 2015 (early)

Global View: All Markets

Global View: All Markets

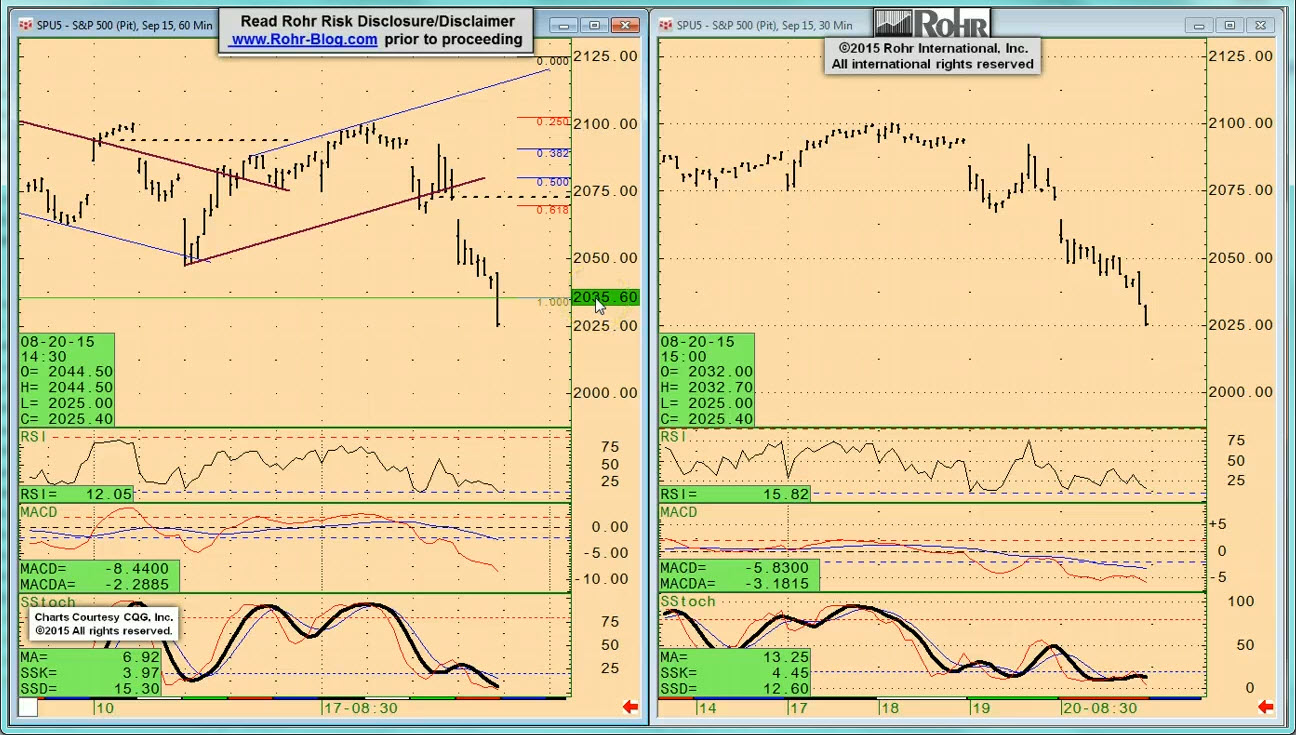

The markets have finally reflected the concerns we have been expressing for some time on the degree to which the cumulative effect of weaker activity in key centers was going to catch up with overly optimistic assessments of the global economy and equities. This is also obviously a positive factor for the fixed income market; especially longer dated government bonds that the Cassandra’s have been warning were in jeopardy of collapsing at any moment due to the imminent central bank rate hikes that were assuredly also going to arrive sooner than not. The renewed ‘tail risk’ is not from some minor economy defaulting on debt or some other influence: It is the potential for all the previous and current central bank Quantitative Easing of the past six years not being enough in and of itself to restore pre-Crisis robust economic growth.

Our previous thoughts on the near term factors regarding that where explored once again in Thursday’s Global View TrendView video analysis post. However, full review of the increasingly troubling extended factors was explored at length in Wednesday afternoon’s Commentary Tail Risk Now Mainstream? post. That was not just our extended opinion, as it also includes a significant number of links to very credible resources. If you have not already done so, we suggest a read to review the confluence of fundamental factors that made potential for the equities selloff (and govvies rally) eminently apparent. That is also important because those same factors may represent a more sustained headwind for the economies and equities than the previous, short-lived setbacks.

And now we are going to do something unusual in proceeding directly to a brief market discussion, leaving that background to our previous extensive analysis.

_____________________________________________________________

Video Timeline: It begins with a macro (i.e. fundamental influences) mention of the key Chinese factor and weak commodities even though some of the data is more balanced once again. Perversely the German Advance Manufacturing PMI came in a bit stronger, yet with the rest of Europe weakish (reflecting recent GDP numbers.) And the Chinese Advance Manufacturing PMI was quite weak with the US a bit softer than expected as well.

It moves on to S&P 500 FUTURE short-term indications at 02:30 and intermediate term view at 04:45, OTHER EQUITIES from 07:30, GOVVIES analysis beginning at 12:00 (with the BUND at 14:45) and SHORT MONEY FORWARDS 18:00. FOREIGN EXCHANGE covers the US DOLLAR INDEX at 21:15, EUROPE at 23:15 and ASIA at 25:00, followed by the CROSS RATES at 28:15 and a return to S&P 500 FUTURE short term view at 31:30. We suggest using the timeline cursor to access the analysis most relevant for you.

_____________________________________________________________

Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion and TrendView Video Analysis and General Update. Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion.

2015/08/25 TrendView VIDEO: Global View (early)

2015/08/25 TrendView VIDEO: Global View (early)

© 2015 ROHR International, Inc. All International rights reserved.

The analysis videos are reserved for Gold and Platinum Subscribers

TrendView VIDEO ANALYSIS & OUTLOOK: Tuesday, August 25, 2015 (early)

While the markets have been wild, on a certain level they have only finally reflected the concerns we have been expressing for some time. That is on the degree to which the cumulative effect of weaker activity in key centers was going to catch up with extensive overly optimistic assessments of global economy and equities prospects. This was also obviously a positive factor for fixed income markets; especially longer dated government bonds that the Cassandra’s have been warning were in jeopardy of collapsing at any moment. That was due to the alleged imminent central bank rate hikes that were assuredly also going to arrive sooner than not. The renewed ‘tail risk’ is not from some minor economy defaulting on debt or some other influence: It is the potential for all the previous and current central bank Quantitative Easing of the past six years not being enough in and of itself to restore pre-Crisis robust economic growth.

That turned up most glaringly in the performance of the Chinese equities of late, yet is a more global potential drag. Our previous thoughts on the near term factors regarding that where explored once again in last Thursday’s Global View TrendView video analysis post. However, full review of the increasingly troubling extended factors was explored at length in last Wednesday afternoon’s Commentary Tail Risk Now Mainstream? post. And that was not just our opinion, as it also includes significant links to very credible resources. We still suggest a read If you have not already done so for the confluence of fundamental factors that made potential for the equities selloff (and govvies rally) eminently apparent. That is also important because those same factors may represent a more sustained headwind for the economies and equities than the previous, short-lived setbacks.

_____________________________________________________________

Video Timeline: It begins with a macro (i.e. fundamental influences) mention of the firming of the recent data (even out of China), including German IFO and exports. However, the key driver of the improvement in European and US equities is the Peoples Bank of China 25 basis point rate to 4.60% with another easing of reserve requirements that will infuse more liquidity. There is some US data today and key end of month data later this week.

It moves on to S&P 500 FUTURE short-term indications at 02:30 and intermediate term view at 04:45, OTHER EQUITIES from 07:30, GOVVIES analysis beginning at 12:00 (with the BUND at 14:45) and SHORT MONEY FORWARDS 18:00. FOREIGN EXCHANGE covers the US DOLLAR INDEX at 21:15, EUROPE at 23:15 and ASIA at 25:00, followed by the CROSS RATES at 28:15 and a return to S&P 500 FUTURE short term view at 31:30. As this is an especially extensive analysis due to volatility factors, even more so than usual we suggest using the timeline cursor to access the analysis most relevant for you.

_____________________________________________________________

Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion and TrendView Video Analysis and General Update. Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion.

Read more...