2015/09/01 TrendView VIDEO: Global View (early)

© 2015 ROHR International, Inc. All International rights reserved.

The analysis videos are reserved for Gold and Platinum Subscribers

TrendView VIDEO ANALYSIS & OUTLOOK: Tuesday, September 1, 2015 (early)

Global View: All Markets

Global View: All Markets

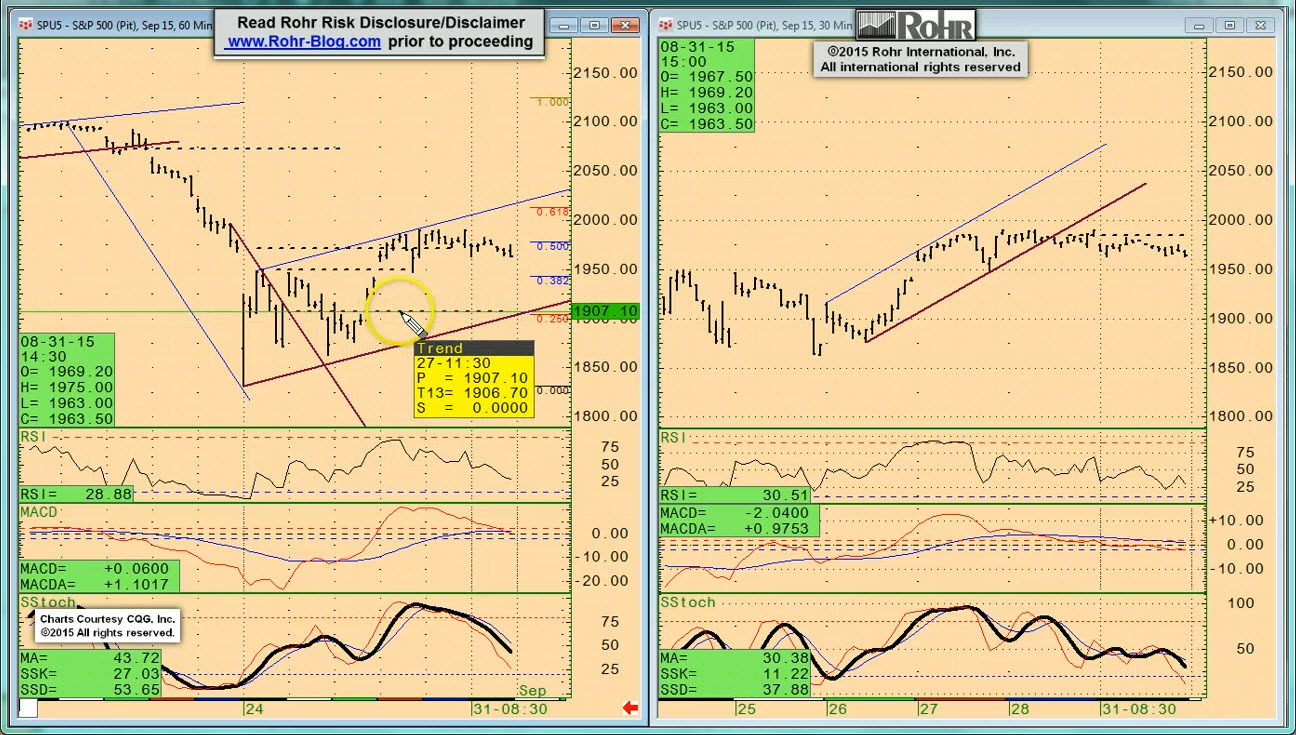

Quite a shockingly lower opening in US equities on the back of weakness elsewhere. This was all ostensibly driven by the weak indication from the Chinese Manufacturing PMI. We don’t believe it. However much the Chinese Caixin number is indeed weak at just 47.30, that is what was indicated by the Advnace PMI release last month. As such it is not a surprise, especially inlight of recent data not providing any reason to believe anything had changed all that much. There were other reaons to be negative this morning, like the Chinese Service PMI weakneing more than expected, even if it remains in modest growth territory (at 51.50 vs. 53.90 last month.) There was also the weakness of Japanese Capital Spending, which throws a bit of doubt on the recently better Japanese economic data.

However, we do not disagree with equities ultimately experiencing a more extensive correction, as has been our “Tail Risk is Back!” theme since our May 2nd post of that title. It is more so whether the equities are going to fall that much farther right now on a reaction to mostly well-anticipated fundamental influences. There is also the matter of the lack of any even remotely equivalent response from the govvies or the foreign exchange. For more on the immediate confluence of negative factors which led to current equities weakness, see our “Tail Risk Now Mainstream?” (rhetorical question) August 19th post.

_____________________________________________________________

Video Timeline: It begins with macro (i.e. fundamental influences) mention of the recent data becoming mixed once again (from somewhat stronger previous), which has been reinforced by this morning’s weakish Manufacturing PMI’s. Yet Chinese Manufacturing was only as soft as the Advance figure. That was after Monday’s positive German Retail Sales but very weak Dallas Fed Index. We have now seen weaker than expected US and Canadian Manufacturing PMI, and as expected US Construction Spending.

It moves on to S&P 500 FUTURE short-term indications at 02:45 and intermediate term view at 05:15, OTHER EQUITIES from 07:45, GOVVIES analysis beginning at 12:00 (with the BUND at 14:45) and SHORT MONEY FORWARDS 16:30. FOREIGN EXCHANGE covers the US DOLLAR INDEX at 19:45, EUROPE at 21:15 and ASIA at 24:15, followed by the CROSS RATES at 26:30 and a return to S&P 500 FUTURE short term view at 30:30. We suggest using the timeline cursor to access the analysis most relevant for you.

_____________________________________________________________

Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion and TrendView Video Analysis and General Update. Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion.

2015/09/04 Commentary: Equities Soggy in Spite of Draghi

2015/09/04 Commentary: Equities Soggy in Spite of Draghi

© 2015 ROHR International, Inc. All International rights reserved.

Extended Trend Assessments reserved for Gold and Platinum Subscribers

COMMENTARY (Non-Video): Friday, September 4, 2015 (early)

Commentary: Equities Soggy in Spite of Draghi

We noted in our last Commentary right after the August 19th FOMC minutes release that the lack of structural reforms has left the global economy less robust than had been hoped and expected. In a nutshell, Quantitative Easing (QE) has not turned near term cyclical economic improvement into sustainable structural economic growth. And why should it? Even as massive as the QE programs in some centers has been (US and Japan) and continues to be (Japan and Euro-zone), it is not a general panacea for weak growth.

This was brought home again yesterday when President Draghi’s opening statement (also including the Q&A transcript at this point) included the announcement of the potential expansion of the amount of assets purchased under the ECB QE program. To wit, “…the Governing Council decided to increase the issue share limit from the initial limit of 25% to 33%, subject to a case-by-case verification…” The market response was obvious in the early (US time) surge in equities with the govvies pushing up as well and the euro currency weakening. For anyone who has not already seen it, the ECB press conference video might be of interest as well.

While the European equities held up through the balance of the day, by later on in the US session the equities had lost their gains. This gets back to the implication we have noted for some time that QE cannot in and of itself return the world to the robust growth last experienced prior to the 2008-2009 financial crisis. And Signore Draghi was also pointed once again that without structural reforms the current QE assisted cyclical recovery will not turn into the growth economy everyone is hoping it will become.

Authorized Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion. Non-subscribers click the top menu Subscription Echelons & Fees tab to review your options and join us. Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to also access the extended trend assessment as well.

Read more...