2015/11/12 TrendView VIDEO: Global View (early)

© 2015 ROHR International, Inc. All International rights reserved.

The analysis videos are reserved for Gold and Platinum Subscribers

TrendView VIDEO ANALYSIS & OUTLOOK: Thursday, November 12, 2015 (early)

Global View: All Markets

Global View: All Markets

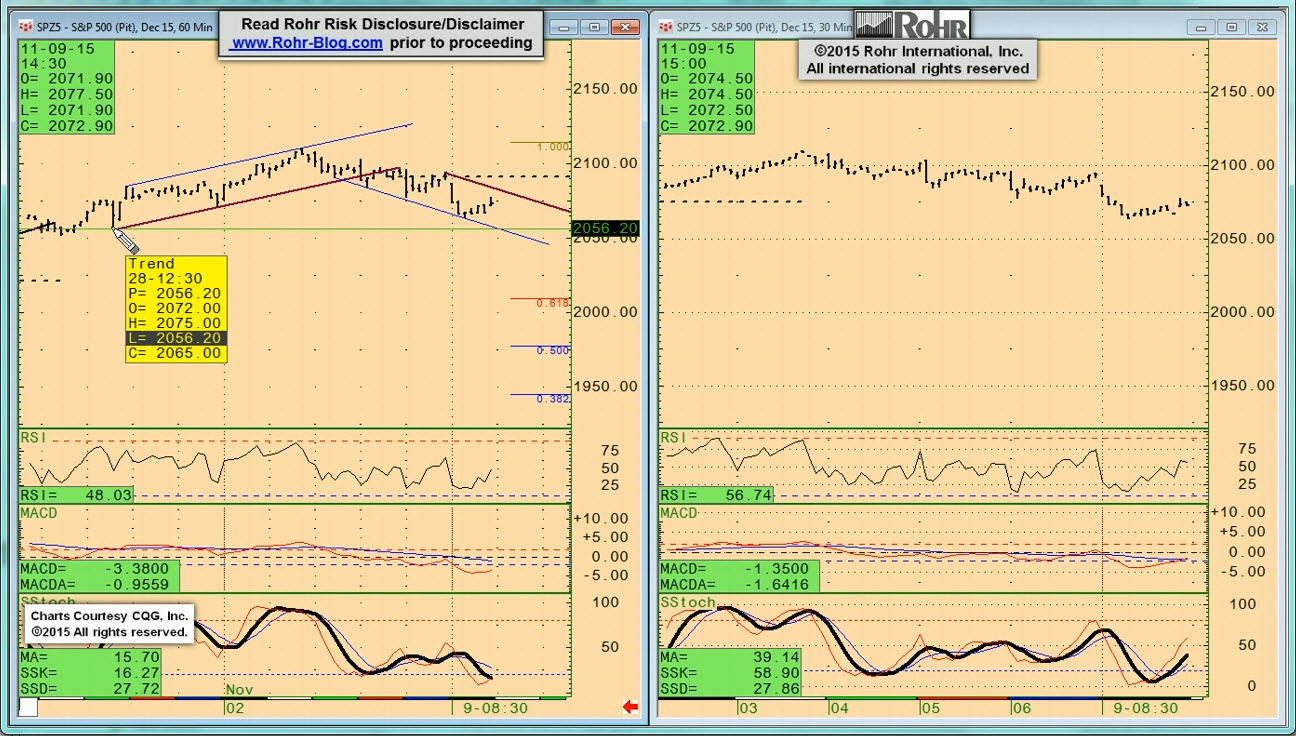

While some weakness might have been expected at some point after Friday’s strong US Employment report, Monday’s drop from the opening after Friday’s December S&P 500 future holding action in the nearby 2,080-75 support. Some might say this is the natural ‘good news is bad news’ influence from the greater potential for and FOMC rate hike in December. While that is possibly the case, the question is why that did not have more of an impact Friday?

There was an entirely different indication Monday morning which may be more so the culprit in the equities slam, US dollar stalling and the govvies stabilization: the OECD (Organization for Economic Cooperation and Development) Economic Outlook and Interim Economic Outlook. And it was quite downbeat, mirroring the slippage into atypical negative outlooks in all of its recent monthly Composite Leading Indicators. If you have not done so already, it is worth a look.

While we will get back to that shortly, there are also central bank cross currents hitting the equities after December S&P 500 future tried to push back above 2,080-75 on Wednesday with no success. ECB’s Draghi was at the European Parliament noting more weakness there than previously acknowledged, yet Janet Yellen was sharing views on post-Crisis Fed monetary policy that left the impression the FOMC was likely ready to finally raise rates at its December meeting. Obviously the combination of worries about Europe and other economies while the Fed seems likely to raise rates is not positive for equities.

_____________________________________________________________

Video Timeline: It begins with macro (i.e. fundamental influences) mention of the strength of the US Employment report coming in the wake of other not so strong data last week. That said, mixed views from central bankers noted above were reinforced by the weak data out of Asia into stronger than expected US Wholesale Sales Tuesday. And positive Employment figures have spread around through Canada, the UK and Australia as well. While that might be a sign that Q4 will be the recovery many have been anticipating, the next key indication is Friday’s US Retail Sales… a key sign of any real consumer recovery.

It moves on to S&P 500 FUTURE short-term at 03:30 and intermediate term view at 05:30, OTHER EQUITIES from 07:00, GOVVIES beginning at 10:30 (with the DECEMBER BUND FUTURE at 13:45) and SHORT MONEY FORWARDS from 15:15. FOREIGN EXCHANGE covers the US DOLLAR INDEX at 17:45, EUROPE at 19:00 and ASIA at 21:30, followed by the CROSS RATES at 24:45 and a return to S&P 500 FUTURE short term view at 29:00. We suggest using the timeline cursor to access analysis most relevant for you.

_____________________________________________________________

Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion and TrendView Video Analysis and General Update. Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion.

2015/11/13 TrendView VIDEO: Concise Highlights (early)

2015/11/13 TrendView VIDEO: Concise Highlights (early)

© 2015 ROHR International, Inc. All International rights reserved.

The analysis videos are reserved for Gold and Platinum Subscribers

TrendView VIDEO ANALYSIS & OUTLOOK: Friday, November 13, 2015 (early)

While some weakness might have been expected at some point after Friday’s strong US Employment report, Monday’s drop from the opening after Friday’s December S&P 500 future holding action in the nearby 2,080-75 support. Some might say this is the natural ‘good news is bad news’ influence from the greater potential for and FOMC rate hike in December. As we have noted all week, there was an entirely different indication Monday morning from the OECD (Organization for Economic Cooperation and Development) Economic Outlook and Interim Economic Outlook. And it was quite downbeat, mirroring the slippage into atypical negative outlooks in all of its recent monthly Composite Leading Indicators. If you have not done so already, it is worth a look.

And that plays right into the central bank cross currents we noted Thursday morning were hitting the equities after December S&P 500 future tried to push back above 2,080-75 on Wednesday with no success. ECB’s Draghi was at the European Parliament noting more weakness there than previously acknowledged, yet Yellen & Co. was sharing views that left the impression the FOMC was likely ready to finally raise rates at its December meeting. Obviously the combination of worries about Europe and other economies while the Fed seems likely to raise rates is not positive for equities. The technical failure in the equities (revisited immediately below) seems a ‘good news is bad news’ function now.

That raises a real question over what the market response might be to the more than a bit critical US Retail Sales report. After sagging on much better US Employment indications last Friday (including the first real improvement in Hourly Earnings for quite some time) and better than expected US Wholesale Sales on Tuesday, will a strong US Retail Sales report be positive for equities? Or will it create more Fed dread regarding December?

_____________________________________________________________

Video Timeline: It begins with macro (i.e. fundamental influences) mention of the factors noted above along with strong Employment figures spreading elsewhere. While that might be a sign that Q4 will be the recovery many have been anticipating, the next key indication will be whether that is constructive for equities if central banks lessen accommodation.

It moves on to S&P 500 FUTURE short-term view at 03:00 and intermediate term at 05:45 with OTHER EQUITIES from 08:45 and only mention of GOVVIES from 12:15 including discussion of the BUND at 13:30, and SHORT MONEY FORWARDS from 14:00. Foreign exchange is also only mentioned, with US DOLLAR INDEX at 14:30, Europe at 15:00, ASIA at 16:00 and CROSS RATES showing weakness of the British pound at 17:00 prior to returning to the S&P 500 FUTURE short term view at 17:45.

_____________________________________________________________

Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion and TrendView Video Analysis and General Update. Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion.

Read more...