2015/11/19 TrendView VIDEO: Global View (early)

© 2015 ROHR International, Inc. All International rights reserved.

The analysis videos are reserved for Gold and Platinum Subscribers

TrendView VIDEO ANALYSIS & OUTLOOK: Thursday, November 19, 2015 (early)

Global View: All Markets

Global View: All Markets

The Minutes Matrix we alluded to yesterday morning did indeed yield the sentiment we expected from the FOMC October meeting. The dominant expectation was they were feeling the economy is strengthening enough to warrant a December meeting hike. Yet it was most interesting that there was also almost as much rate hike dissent at the October meeting as we saw in September. This was reinforced by Cleveland Fed President Mester’s appearance on CNBC this morning. When asked whether she was ‘dove’ or ‘hawk’, she responded that she was an ‘owl’. In other words, there are likely others like her on the FOMC who remain more ‘data dependent’ than the hawks would like to believe.

And as we have noted for some time in the wake of the much weaker economic data since last, quite strong US Employment report, there is good reason to question if December will indeed be the right window for the Fed to put through that first rate hike in nine years. Noted repeatedly of late is last Monday morning’s OECD Semi-annual Outlook. The bottom line is that much of the world including the US is less constructive than recent Fed views, still led by China and emerging economies. Yet that includes the prescient indication Japan was weakening again, and the UK remaining weak as well. The idea Europe is strengthening is only in the context of how weak it was.

[NOTE: We updated the Market Observations below Wednesday’s Concise Highlights TrendView video analysis early this morning for the benefit of any subscribers who wanted to see our post-FOMC minutes assessment prior to this morning’s video analysis. Those remain our views, and they are posted once again below the video in this post.]

_____________________________________________________________

Video Timeline: It begins with macro (i.e. fundamental influences) mention of the factors noted above, and we note the equities recent failure was in spite of recent strong US Employment figures spreading elsewhere. While that might have been a sign Q4 will be the long anticipated recovery, recent indications at the end of last week and this week are less constructive, including much of the data and Japan sinking back into recession.

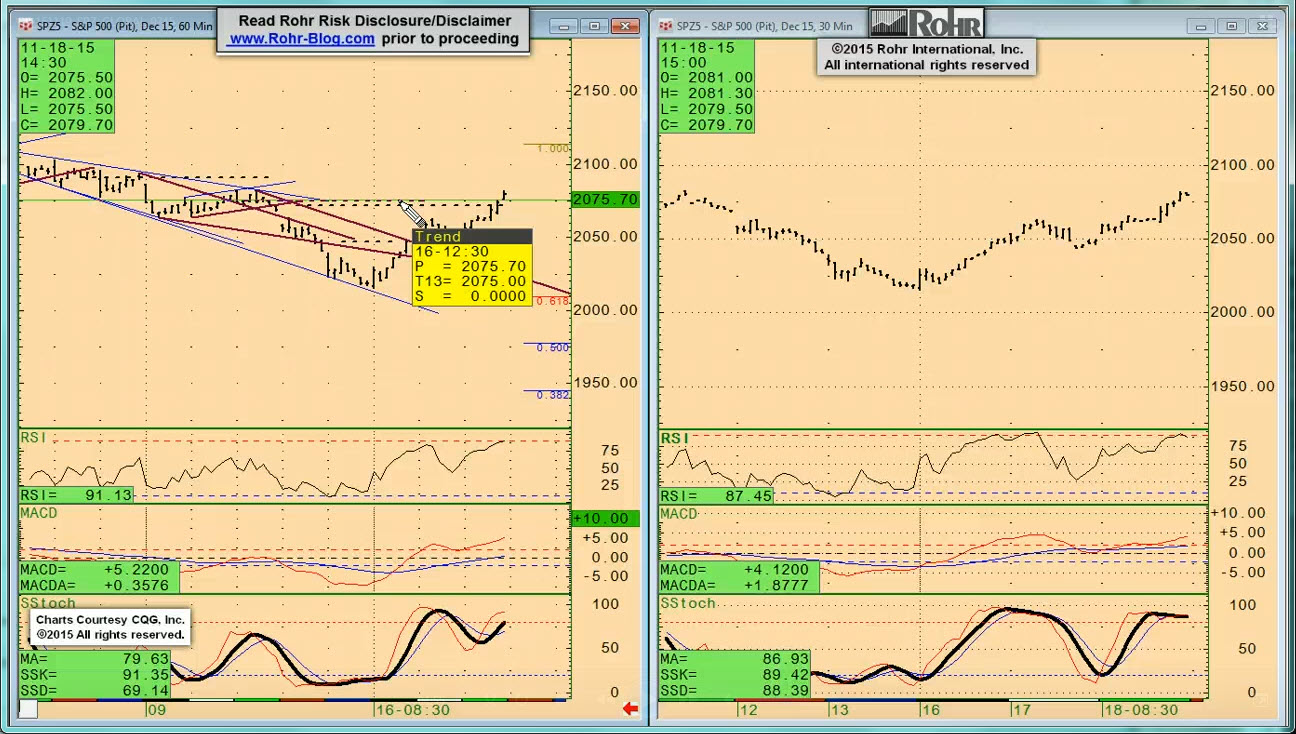

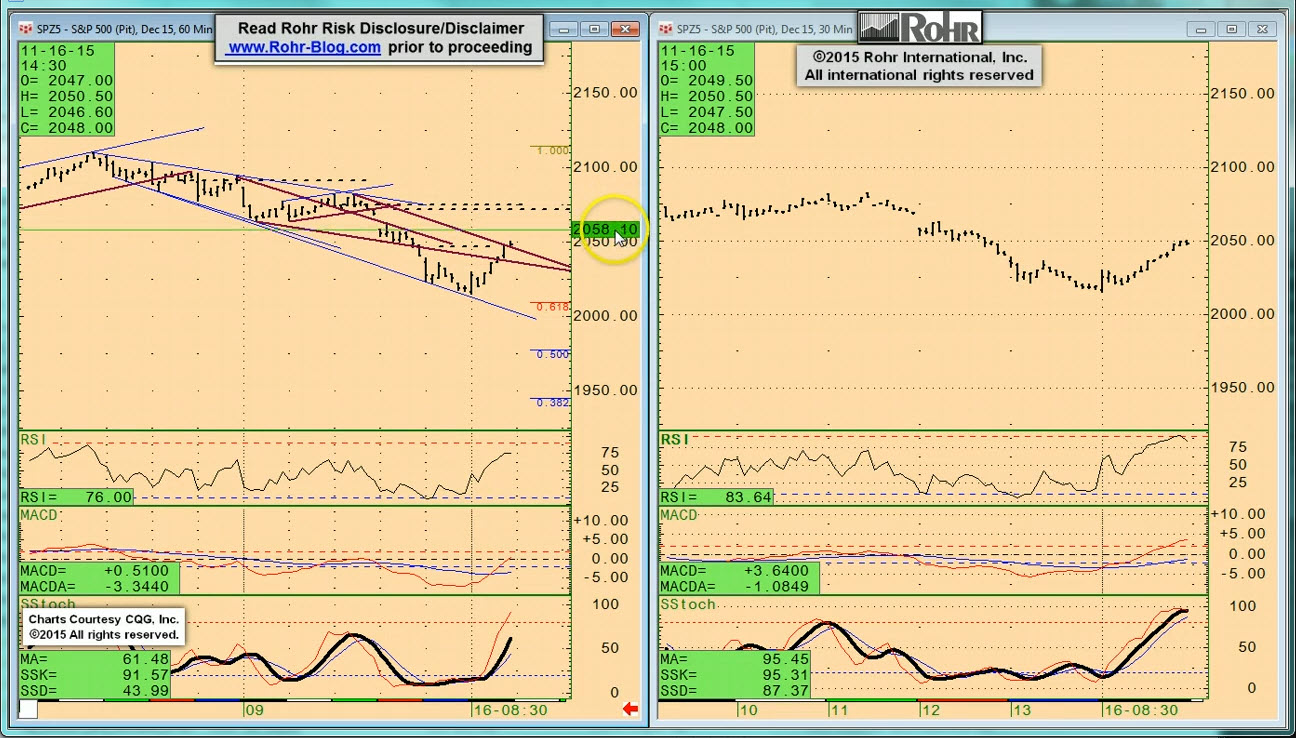

It moves on to S&P 500 FUTURE short-term at 03:00 and intermediate term view at 05:30, OTHER EQUITIES from 07:45, GOVVIES beginning at 11:00 (with the DECEMBER BUND FUTURE at 14:00) and SHORT MONEY FORWARDS from 15:45. FOREIGN EXCHANGE covers the US DOLLAR INDEX at 18:30, EUROPE at 20:15 and ASIA at 23:00, followed by the CROSS RATES at 26:00 and a return to S&P 500 FUTURE short term view at 29:45. We suggest using the timeline cursor to access analysis most relevant for you.

_____________________________________________________________

Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion and TrendView Video Analysis and General Update. Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion.

2015/11/20 TrendView VIDEO: Concise Highlights (early)

2015/11/20 TrendView VIDEO: Concise Highlights (early)

© 2015 ROHR International, Inc. All International rights reserved.

The analysis videos are reserved for Gold and Platinum Subscribers

TrendView VIDEO ANALYSIS & OUTLOOK: Friday, November 20, 2015 (early)

The FOMC October meeting minutes yielded the sentiment we (and many others) expected. There was the expression the US economy is strengthening enough to warrant a December meeting hike. Yet it was most interesting that there was also almost as much rate hike dissent in the form of reliance on “continued improvement in conditions” at the October meeting as we saw in September. This was reinforced by Cleveland Fed President Mester’s appearance on CNBC Thursday morning. When asked whether she was ‘dove’ or ‘hawk’, she responded that she was an ‘owl’. In other words, there are likely others like her on the FOMC who remain more ‘data dependent’ than the hawks would like to believe.

And as we have noted for some time in the wake of the much weaker economic data since the last, quite strong US Employment report, there is good reason to question if December will indeed be the right window for the Fed to put through that first rate hike in nine years. Noted repeatedly of late is last Monday morning’s OECD Semi-annual Outlook. The bottom line is that much of the world including the US is less constructive than recent Fed views, still led by China and emerging economies. Yet that includes the prescient indication Japan was weakening again, and the UK remaining weak as well. The idea Europe is strengthening is only in the context of how weak it was. And the recent data and expressions of concern belie any expectations of real strength.

And the real influence back into the markets was going to be whether they believe the US economy is indeed still getting stronger in the wake of economic data that has softened again since the Employment report into weaker than expected US Retail Sales last Friday. On current form, the strength of equities doesn’t feel like it is driven by strong data, and the other asset classes are conforming to that weaker view (more below.)

_____________________________________________________________

Video Timeline: It begins with macro (i.e. fundamental influences) mention of the factors noted above, with recent signs Q4 will not be the anticipated recovery. In addition to other factors, Monday’s GDP showed Japan back in recession, this morning’s Chinese Leading Indicators and Canadian Retail Sales (mimicking the US) were also still quite weak.

It moves on to S&P 500 FUTURE short-term view at 03:00 and intermediate term at 05:45 with OTHER EQUITIES from 08:00 and only mention of GOVVIES from 09:15 including discussion of the BUND at 11:00, and SHORT MONEY FORWARDS from 11:45. Foreign exchange is also only mentioned, with US DOLLAR INDEX at 12:30, Europe at 13:30, ASIA at 14:45 and CROSS RATES that are mostly steady yet with a weak euro at 16:15 prior to returning to the S&P 500 FUTURE short term view at 16:45.

_____________________________________________________________

Authorized Gold and Platinum Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion and TrendView Video Analysis and General Update. Silver and Sterling Subscribers click ‘Read more…’ (below) to access the balance of the opening discussion.

Read more...